In our previous blog post, we updated the PQC USPS corporate brand valuation model with FY2014 data. The result ($6.23 billion) is a considerable increase over the value computed using the FY2013 data. In this blog post we consider why the value increased and whether the increase is reasonable.

A review of the financial data indicates that the large increase in brand value is due to volatility and changes in several balance sheet liabilities that are critical pieces when normalizing the operating income in the residual income approach. These include:

- The FY2013 financial data included a $1.32 billion one-time adjustment for a deferred revenue liability. No such adjustment exists in FY2014.

- The other adjustment is a recurring item, where the long-term workers’ compensation adjustment is significantly different (and flips sign) in FY2014 compared to FY2013. The primary reason is due to discount rate changes related to workers’ compensation liability.

These two adjustments have the cumulative effect of yielding a FY2014 “normalized” income stream that is 58 percent higher than the FY2013 normalized income stream. Herein we explore the value difference issue, where the mechanical application of the residual income approach ignores the need to apply sound judgment year to year when implementing the approach. As we continue through the computation , the net effect is that brand-level cash flows (i.e., the residual) and thus, brand value, are also significantly higher when using FY2014 data compared to FY2013 data (and holding all other assumptions constant). This increase begs the question whether the higher GAAP adjusted profits truly translate to a 72 percent increase in the corporate brand value!

Does this mean that our initial brand valuation model and results are invalid? In our opinion the answer to this question is no, understanding that the FY2014 results are a formulaic output without considering the reasonableness of the normalized income stream in light of year to year changes. If anything, the FY2014 analysis allows us to revisit the formulaic approach and assumptions within the residual income approach to help calibrate the model with respect to inputs.

For the two major adjustments discussed above, we consider the following alternatives:

- The deferred revenue adjustment was booked in FY2013, yet has applicability to the estimated liability for “Forever” stamps sold in multiple prior years. One alternative treatment is to amortize the deferred revenue adjustment over several years to smooth the effect on this one time change in an accounting estimate.

- The long-term workers’ compensation adjustment exhibits tremendous volatility on a year-to-year basis. In order to control and help smooth out this volatility, one alternative is to look at a multi-year average to include as the adjustment (e.g., three-year rolling average adjustment). So instead of backing out a negative 310 million adjustment in FY2013 and a positive $1,180 million adjustment in FY2014, we look at what the average adjustment is in the three years prior to and including our particular year.

By examining multi-year financial data for normalizing adjustments, we are able to smooth out the financial volatility that can yield potentially anomalous results once input into the purely formulaic residual income approach.

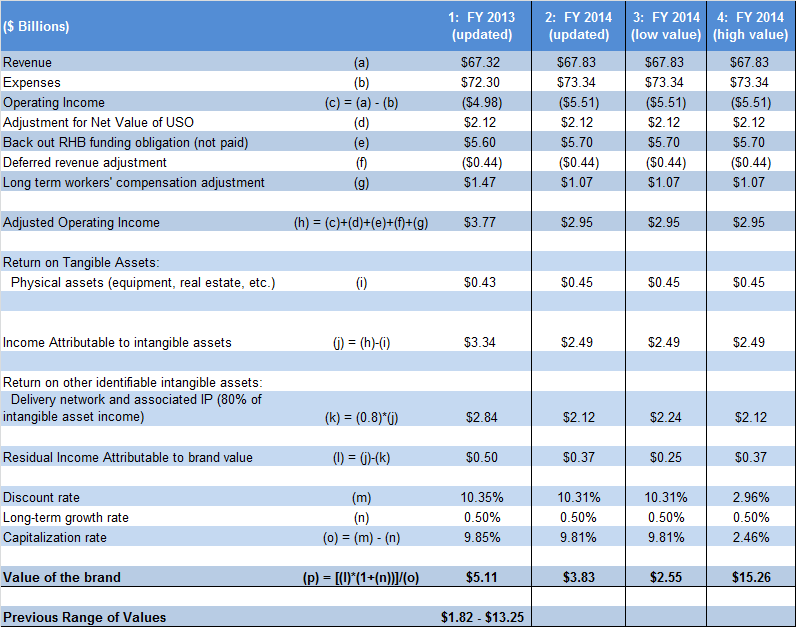

However, we also need to consider other valuation assumptions, which we deferred on in our prior blog post and update (setting the stage for this blog post!). In our original valuation model and white paper, we relied upon Postal Regulatory Commission (PRC) estimates for the net value of the universal service obligation (USO). At the time, we did not have 2013 estimates and we relied on 2012 estimates. The PRC has since updated the calculations, allowing us to include the 2013 estimates in our original model, while also relying on these values for 2014 (as the PRC has not released a 2014 estimate as of yet). Table 1 provides a comparison of the FY2013 and FY2014 brand value calculations using the residual income approach but with a multi-year average for the normalizing adjustments (#1 and #2 above) and updating the USO estimate. These are shown in the first two computational columns of Table 1.

In examining the first two columns of Table 1, we note that updating the FY2013 brand value calculations leads to an increase (from our prior $3.63 billion to $5.11 billion), while the FY2014 brand value is now lower than the FY2013 value.

So what is the “right” answer?

The answer is not necessarily a straightforward point estimate. This is particularly true given our use of historical data as a proxy for a forward-looking income stream. In an ideal world, we might have proprietary brand cash flow or other financial projections, expectations and strategies to incorporate in our model. Absent the forecast element, we rely on historical data to forecast the future, which lends support to expressing a range of values given the limitations raised by the model constraints (e.g., use of public data, transparent and easily reproducible).

Nevertheless, in our original white paper we noted the significant influence of key valuation assumptions such as the identification and impact of brand attributes on brand equity and value. Furthermore, the assessment of brand risk and importance of other intangible assets also influence the overall corporate brand value. In our previous blog post we conveniently ignored an assessment of those elements in presenting our updated calculation by simply using FY2014 data in the model, thereby setting the stage for this discussion. But valuation is not a mechanistic approach, as it requires judgment and the consideration of alternative assumptions. In our original white paper, we presented a range of values based on sensitivity analyses regarding different inputs. In columns 3 and 4 of Table 1, we present a similar “low” and “high” case using the updated FY2014 model to illustrate a similar range of values.

Ultimately, the updated brand valuation also needs to assess how the critical brand attributes might have changed from one year to the next, where we evaluate the potential changes in consumer perceptions and buying behavior. A more negative view will increase the risk the brand cash flows will be realized, which can be reflected in the residual cash flows and/or the discount rate. We should also consider any change in the perception of the importance of other tangible and intangible assets (e.g., delivery network), such that we might revise our estimates of the return on tangible assets or the profit split between the delivery network, other IP and the brand.

Need help with a brand valuation and assessment? Have a question about valuation? Let us know!